How to Budget by Paycheck Without Overcomplicating It

Introduction

A monthly budget can look fine on paper and still feel stressful in real life.

That often happens because the budget does not match your paycheck timing.

You may technically have enough income for the month, but if too many bills are due before the next paycheck, the first half of the month can feel tight. Then the second paycheck has to cover everything that is left.

That is where paycheck budgeting helps.

A paycheck budget breaks the month into smaller pieces. Instead of only asking, “Can I afford this month?” you ask, “What does this paycheck need to cover before the next one arrives?”

Here is a simple way to do it without making your budget more complicated than it needs to be.

What Is a Paycheck Budget?

A paycheck budget is a plan for one paycheck at a time.

It tells you how much money is coming in, what bills are due before the next paycheck, what essentials need to be covered, and how much room is left for flexible spending or savings goals.

A paycheck budget is especially helpful if you are paid:

- weekly

- every two weeks

- twice a month

- irregularly

- from multiple income sources

It can also help if your bills are not evenly spread across the month.

Step 1: Write Down Your Paycheck Date and Amount

Start with the paycheck you are planning.

Write down:

- paycheck date

- expected take-home pay

- any extra income expected before the next paycheck

- the date of your next paycheck

Use take-home pay, not gross income. Your budget needs the amount that actually lands in your account.

If your income changes, use a conservative estimate. It is better to plan with a lower number and adjust upward later than to assume money will arrive and feel squeezed if it does not.

Step 2: List Bills Due Before the Next Paycheck

Next, look at the bills due between this paycheck and the next one.

Examples include:

- rent or mortgage

- utilities

- phone

- internet

- insurance

- car payment

- credit card minimums

- subscriptions

- childcare

- loan payments

Write the due date and amount next to each one.

This step matters because not every bill belongs to every paycheck. If a bill is due before the next paycheck arrives, this paycheck needs to cover it.

Step 3: Add Essentials for This Pay Period

After bills, list the essentials you need before the next paycheck.

Common essentials include:

- groceries

- gas or transportation

- household supplies

- pet food

- prescriptions

- basic personal care

Try to estimate what is realistic for the number of days this paycheck needs to cover.

For example, if this paycheck has to cover two full weeks of groceries, do not use a one-week grocery estimate. Paycheck budgeting works best when the timeline is honest.

Step 4: Plan Flexible Spending

Flexible spending is the money that can move around more easily.

This might include:

- eating out

- coffee

- entertainment

- clothing

- hobbies

- small gifts

- personal spending

You do not have to remove flexible spending completely. In fact, a budget that leaves no room for real life is hard to follow.

The goal is to choose a limit before the money disappears by accident.

Step 5: Include Sinking Funds

If you are working on sinking funds, include them in the paycheck plan.

A sinking fund is money set aside for an expense you know is coming later.

Examples:

- car maintenance

- annual bills

- holidays

- school supplies

- medical costs

- home repairs

- pet care

- travel

You may not be able to fund every category from every paycheck, and that is okay. Choose the most important ones first.

Even small amounts can make future expenses less stressful.

Step 6: Leave a Buffer if You Can

A paycheck budget should include a small buffer whenever possible.

A buffer can help cover:

- a bill that is a little higher than expected

- an extra grocery item

- gas price changes

- a forgotten small expense

- timing issues between transactions

The buffer does not need to be large. Even a small amount can help prevent overdrafts or extra stress.

If you cannot add a buffer right now, simply make it a future goal.

Step 7: Check What Is Left

After you subtract bills, essentials, flexible spending, sinking funds, and buffer money, look at what remains.

If the number is negative, do not panic. That is useful information.

Ask:

- Can a flexible category be lowered?

- Can a bill be moved to another paycheck?

- Is there a subscription to pause or cancel?

- Does the next paycheck have more room?

- Do I need to adjust my monthly estimates?

The point of a paycheck budget is to catch problems before they happen.

Example Paycheck Budget Flow

Here is a simple flow you can follow:

- Paycheck amount

- Bills due before next paycheck

- Groceries and essentials

- Gas or transportation

- Sinking funds

- Flexible spending

- Buffer

- Remaining amount

This keeps the plan clear without requiring complicated formulas.

Common Paycheck Budgeting Mistakes

Mistake 1: Planning the whole month from one paycheck

If you use the first paycheck to cover too much, the second half of the month can feel tight. Assign bills based on due dates.

Mistake 2: Forgetting groceries and gas

Bills are obvious, but essentials are where budgets often get squeezed. Give them a realistic estimate.

Mistake 3: Ignoring subscriptions

Small charges can stack up. Include subscriptions in the paycheck where they renew.

Mistake 4: Leaving no buffer

A zero-dollar plan can look neat, but real life needs breathing room.

Paycheck Budget Checklist

Use this quick checklist each time you plan a paycheck:

- Write the paycheck date

- Write expected take-home pay

- List bills due before the next paycheck

- Estimate groceries and essentials

- Add gas or transportation

- Add sinking funds if possible

- Choose flexible spending limits

- Add a small buffer

- Check what is left

- Adjust before the pay period starts

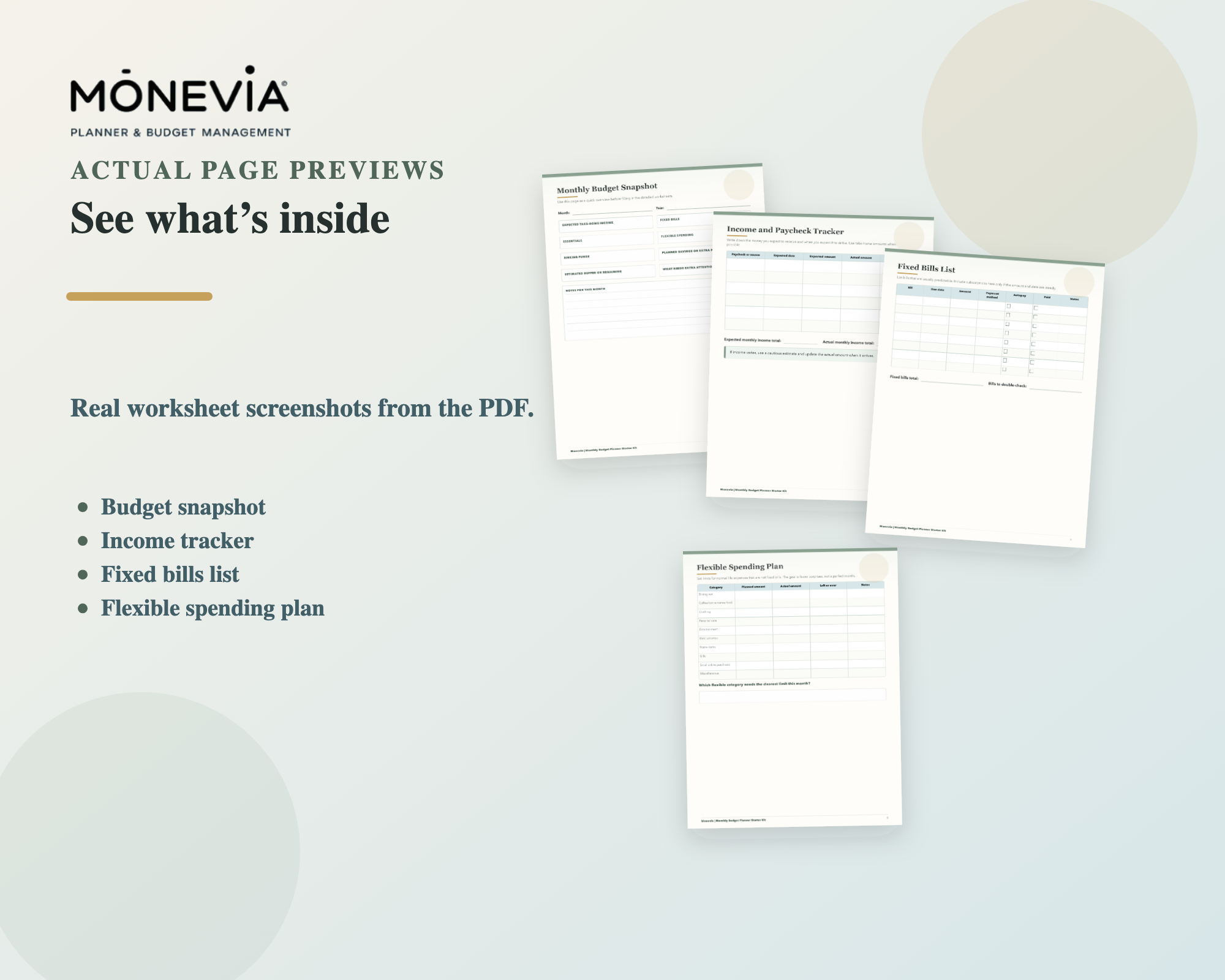

A Printable Paycheck Budget Planner

The Monthly Budget Planner Starter Kit includes paycheck budget worksheets designed to help you plan what each paycheck needs to cover.

It also includes pages for fixed bills, essentials, flexible spending, sinking funds, subscriptions, and monthly reset planning.

Use it when you want a simple printable way to see your paycheck plan before the money starts moving.

Final Thoughts

Paycheck budgeting is not about making your money life more complicated.

It is about matching your budget to the way money actually arrives and leaves.

When you know what each paycheck needs to cover, you can make better decisions before the pay period gets busy.

This article is for educational and organizational purposes only. It is not personalized financial, legal, tax, credit, investment, or debt advice. No specific financial outcome is guaranteed.